Medicare can feel complicated, leaving many people with questions about how it works. We’re here to help make sense of it all. In this guide, we’ll answer the top 10 most common questions about Medicare. Our goal is to provide clear and simple explanations that empower you to understand your options. From understanding the different parts of Medicare to recognizing the importance of Medigap, we’ve got you covered. Dive in to get the answers you need, so you can feel confident in your Medicare decisions. Remember, our site is a resource to guide you through this journey.

Compare Medicare Plans

Compare plans and costs in your area

Common Medicare Questions Answered

Key Highlights

- Medicare Parts A and B cover hospital and outpatient services, forming the backbone of the program.

- Medicare Open Enrollment runs from October 15 to December 7, making it essential to remember these key dates.

- Choosing the right Medicare plan depends on your healthcare needs, services, and budget considerations.

- Medicaid differs from Medicare, serving low-income individuals with broader coverage options.

- Regularly reviewing Medicare Summary Notices helps prevent abuse and protect your benefits.

Compare plans and enroll online

What is Medicare and How Does it Work?

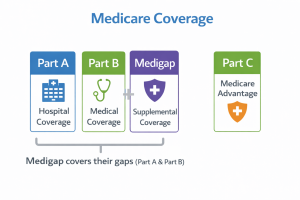

Medicare is a crucial program helping millions of Americans aged 65 and older manage their healthcare needs. Understanding Medicare coverage can seem daunting initially, but breaking it down makes it simpler. The Medicare program is divided into parts, each offering distinct benefits. Original Medicare includes Part A, covering hospital services, and Part B, which handles outpatient services and doctor visits. Many choose to supplement these with additional plans, such as Medicare Advantage or Medigap, to cover potential gaps. Knowing how these pieces fit together helps you better navigate your healthcare options.

I am text block. Click the edit button to change this text. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

Understanding the Basics of Medicare Coverage

Medicare coverage involves several parts, each designed to handle specific healthcare needs. Original Medicare primarily includes Part A and Part B. Part A is your hospital insurance, covering inpatient hospital stays, care in a skilled nursing facility, hospice care, and some home healthcare. Part B, on the contrary, is your outpatient care, covering services like doctor visits, outpatient care, and preventive services. Together, they form the backbone of the Medicare program. However, many find that these basic parts may not cover all their healthcare needs. That’s where supplemental insurance comes into play. You can choose additional plans like Medicare Advantage (Part C) or Medigap policies to help cover what original Medicare doesn’t. Medicare Advantage plans are offered by private companies approved by Medicare, bundling Part A and Part B coverage, often with additional benefits like dental, vision, and hearing services. Medigap, on the other hand, assists with costs like copayments and deductibles not covered by Original Medicare. Deciding which parts and plans suit your needs best involves considering your healthcare requirements and budget. Ensuring you have the right Medicare coverage will ensure you’re not unexpectedly paying for services out-of-pocket.

To expand on understanding Medicare coverage, consider these key factors when evaluating your supplemental insurance options:

- Examine your current and potential future healthcare needs thoroughly.

- Compare the benefits of Medicare Advantage and Medigap carefully.

- Review the providers’ networks and coverage area limitations.

- Assess additional services like dental, vision, and hearing in plans.

- Evaluate plan costs beyond premiums, including potential out-of-pocket expenses.

- Look into customer service ratings and user experiences with plan providers.

- Confirm any enrollment periods or eligibility requirements applicable.

This list can guide you in making more informed Medicare coverage decisions while being mindful of individual needs.

When is Medicare Open Enrollment?

Medicare Open Enrollment is a key period each year when you can review and adjust your Medicare plans. This time is crucial as it allows beneficiaries to enroll or make changes to their Medicare Advantage, Part D prescription drug plans, and supplemental insurance. Understanding the dates and deadlines of the enrollment period can help you ensure your coverage meets your health needs and budget effectively. Being well-prepared during this period can save you from unexpected out-of-pocket costs and ensure you’re making the best decisions about your healthcare coverage.

Key Dates You Need to Remember

The Medicare Open Enrollment Period occurs annually from October 15 to December 7. This timeframe is vital because it’s when you can enroll or make changes to your Medicare plans. During the enrollment period, you have the option to switch from Original Medicare to a Medicare Advantage plan, change from one Medicare Advantage plan to another, or modify your Part D prescription drug coverage. Keeping these dates in mind ensures you make timely decisions that help maintain or improve your healthcare coverage without facing coverage gaps. To stay informed, consider using resources like a live chat with Medicare experts or finding local organizations that can help answer your Medicare questions. Planning ahead during the enrollment period helps in choosing the right plan and avoids potential out-of-pocket costs later. Remember that after December 7, your next opportunity to make changes won’t come until the next enrollment period unless you qualify for a Special Enrollment Period. By understanding these key dates, you can proactively manage your Medicare enrollments and ensure your healthcare needs are adequately covered.

How Do I Know What Medicare Coverage is Right For Me?

Deciding on the right Medicare coverage is essential for your healthcare journey. With various plans and benefits available, it can be overwhelming to choose what fits best. It’s important to compare Medicare plans, weighing the pros and cons of Original Medicare and other options like Medicare Advantage and Medigap. Evaluate your healthcare needs, services that matter to you, and the providers you prefer. By understanding these elements, you can select a Medicare plan that aligns with your health and financial goals.

Comparing Different Medicare Plans and Benefits

When it comes to comparing different Medicare plans and benefits, understanding the nuances of each option is key. Original Medicare consists of Part A and Part B, which cover hospital services and outpatient services like doctor visits, respectively. However, many seniors find that these parts don’t cover everything they might need. This is where comparing Medicare Advantage plans becomes important. These plans, offered by private providers, bundle Part A and Part B coverage and typically include additional benefits not covered by Original Medicare, such as dental, vision, and even hearing services.

In contrast, Medigap policies, also known as supplemental insurance, fill financial gaps in Original Medicare, like copayments and deductibles, giving you financial peace of mind. When deciding, consider what services you prioritize most and how they align with the advantage plan or supplemental insurance you’re considering. It’s also vital to check for healthcare providers within the plan’s network and any budget concerns. By thoroughly comparing your Medicare coverage options, you can choose a plan that supports your health and well-being.

How Much Do Medicare Costs and Premiums Affect My Budget?

Understanding how Medicare costs fit into your budget is vital as you plan for healthcare expenses. Medicare involves premiums, out-of-pocket costs, and sometimes, supplemental insurance. Each of these plays a significant role in how much you’ll spend on healthcare. It can be helpful to look at your annual budget and check where medical expenses fit. Doing so helps ensure there’s room for premiums and unexpected costs. Knowledge about these costs empowers you to make informed choices, helping you prepare for healthcare expenses now and in the future.

Understanding Medicare Premiums and Other Costs

Medicare premiums are one of the primary costs you’ll encounter. For Medicare Part B, premiums are typically deducted from your Social Security benefits, while premiums for Medicare Advantage or Part D require separate payments. Along with premiums, there are out-of-pocket costs like deductibles and copayments, which can vary based on your chosen plan. Original Medicare, including Part A and Part B, covers certain health services, but you might need supplemental insurance to cover potential gaps. Medigap policies are often preferred for this because they help manage out-of-pocket expenses, but they also come with premiums. Balancing these costs is crucial for maintaining a healthy budget.

When assessing Medicare costs, consider additional supports like Medicaid if you’re eligible, which can help with premiums and other expenses. Remember, knowledge about your benefits is equally important. Each decision impacts your budget and coverage, from choosing the right plan to understanding what Medicare benefits cover. By keeping informed and regularly evaluating how Medicare fits into your budget, you can manage costs effectively. This proactive approach means you’re better equipped to handle healthcare expenses without financial strain.

| Cost Type | Components | Coverage Source | Budget Strategy |

|---|---|---|---|

| Premiums | Monthly payment for Medicare Part B, Part D, or Advantage Plan | Government and private insurers | Allocate a monthly budget to cover ongoing expenses |

| Deductibles | Annual amount before coverage starts | Primarily Medicare Parts A and B | Plan for annual healthcare spending threshold |

| Copayments/Coinsurance | Out-of-pocket payment for services | Medicare-approved providers | Include variable expenses in the budget |

| Out-of-Pocket Maximum | Spending cap on expenses in Medicare Advantage | Set by insurance providers | Utilize savings to cover potential expenses up to the cap |

This table provides an overview of how Medicare costs are structured and their implications for personal budgeting.

Find & Compare Plans Online

What Does Medicare Cover for Prescription Drug Needs?

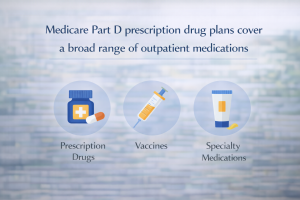

When you’re considering Medicare coverage for prescription drugs, it’s essential to know how different plans can meet your medication needs. Medicare offers options specifically for this through Medicare Part D and Medicare Advantage plans with drug coverage. Understanding how these plans work helps you avoid unexpected costs while ensuring you get the medications you need. By comparing different plans available in your area, you can find the right fit for your prescription drug requirements and budget. It’s crucial to assess these options carefully to ensure comprehensive and affordable coverage.

Exploring Medicare Part D Options

Medicare Part D is a crucial option for anyone who needs prescription drug coverage. It helps cover the cost of medications, providing relief from the financial burden of paying for prescriptions out-of-pocket. With Part D, each plan is offered by private insurance companies and can differ by state, so exploring the available options in your area is necessary. Each prescription drug plan under Part D has a formulary, a list of covered drugs, which can differ significantly between plans. This is why comparing the formulary of each plan is vital to ensure your prescriptions are covered. Part D plans also vary based on premiums, copayments, and deductibles. Knowing the specific costs associated with each plan helps you find one that aligns with your financial situation and drug needs. Additionally, Part D is often integrated into Medicare Advantage (Part C) plans, which combine health coverage with drug coverage in one plan. As you explore your options, pay attention to these details to ensure your prescription drug costs are manageable and that all your necessary medications are covered properly by Medicare.

Who is Eligible for Medicare and How to Enroll?

Understanding who qualifies for Medicare and the steps to enroll can make navigating your healthcare choices smoother. Generally, adults 65 and older or individuals under 65 with certain disabilities are eligible for Medicare. Enrollment involves specific timelines and guidelines, ensuring you’re covered without facing penalties. Knowing these guidelines helps safeguard your access to the necessary health services. From initial eligibility to Medicare coverage choices, grasping the enrollment process is crucial for obtaining comprehensive healthcare services and understanding your coverage options.

Guidelines for Eligibility and Enrollment

The Medicare program lays out clear guidelines for eligibility and enrollment. To qualify, most people must be 65 or older, although younger individuals with specific disabilities or end-stage renal disease are also eligible. Your eligibility begins three months before your 65th birthday and extends until three months after, forming your initial enrollment period. During this time, you should enroll in Medicare Parts A and B. Part A typically covers hospital services, while Part B includes outpatient services. If you’re already receiving Social Security benefits, you might be automatically enrolled. However, if you’re not, you’ll need to enroll yourself. This enrollment ensures you have medical coverage when you turn 65 or qualify otherwise. Missing this initial window could mean late enrollment penalties, impacting your overall Medicare coverage. For those who continue working past 65 with employer coverage, there are special enrollment periods, ensuring a transition to Medicare without penalties. Successfully navigating these guidelines for eligibility and enrollment secures your Medicare services, whether it’s hospital care, outpatient visits, or accessing medical equipment under Medicare coverage. Understanding these Medicare enrollment rules is essential for your healthcare journey, ensuring you maximize the benefits available from your Medicare options.

How Can I Get Dental, Vision, and Hearing Coverage with Medicare?

Finding dental, vision, and hearing coverage through Medicare requires understanding which services are included and exploring additional options. Original Medicare, covering hospital and outpatient services, doesn’t typically include these specific benefits. Many seniors look to Medicare Advantage plans or supplemental insurance plans to fill this gap. These plans, offered by private providers approved by Medicare, can include additional services to meet various health needs. Knowing how to leverage available options ensures that critical services, like regular dental cleanings and eye exams, are accessible without unexpected costs.

Exploring Available Ancillary Product Options

When considering how to get dental, vision, and hearing coverage, exploring the available ancillary product options is key. While Original Medicare does not cover these services, there are several ways to access them. One popular approach is through a Medicare Advantage plan, which often includes additional benefits that Original Medicare doesn’t cover. These plans may offer dental cleanings, eye exams, and even hearing aids as part of their coverage. It’s important to carefully review what’s included in each Medicare Advantage plan, as plans can greatly vary in terms of services and costs. Another option is to purchase stand-alone dental, vision, and hearing insurance policies. These supplemental insurance products can be tailored to your needs, providing flexibility in coverage and costs. Check with various providers to see what options might suit your specific health needs the best. Additionally, consider providers that offer bundled services, balancing both premiums and out-of-pocket expenses. By exploring these ancillary product options, you can ensure your comprehensive health needs are met beyond what standard Medicare plans offer, making your healthcare package both effective and affordable. Remember, taking the time to research these options will help keep your smile bright, your eyesight clear, and your hearing sharp for years to come.

Is There a Difference Between Medicare and Medicaid?

Understanding the distinction between Medicare and Medicaid is vital for choosing the right healthcare coverage. While both programs provide essential health benefits, they serve different purposes and populations. Medicare offers a range of healthcare services primarily for older adults aged 65 and older, along with some younger individuals with disabilities. Original Medicare, for example, includes hospital and outpatient services. Medicaid, on the other hand, focuses on providing healthcare to those with limited income, often covering a wider array of services compared to Medicare. Knowledge of these differences helps in selecting appropriate plans and benefits.

Understanding How These Programs Serve Different Needs

Medicare and Medicaid are often mentioned together, but they cater to distinct groups with unique needs. Medicare is primarily aimed at individuals 65 and over or those with specific disabilities, granting access to healthcare through a structured plan known as Original Medicare. This includes Part A for hospital services and Part B for outpatient and doctor visits. In contrast, Medicaid serves individuals and families with limited income and resources, providing comprehensive health coverage, often extending beyond what Medicare covers. This can include more extensive dental, vision, and hearing services, as well as long-term care.

Medicaid’s ability to cover these additional services makes it integral for those needing more exhaustive benefits. Medicaid operates with both state and federal involvement, meaning services and eligibility criteria can vary by state. This flexibility allows Medicaid to adapt its providers and services according to local needs, making it particularly beneficial for diverse populations. Understanding these programs ensures you make informed choices based on your specific health requirements and financial situation. Comparing the nature of these plans, alongside your own healthcare priorities and budget, is key to navigating the broader landscape of healthcare coverage effectively.

What Resources Help Prevent Medicare Abuse?

Medicare abuse can threaten the effectiveness of your coverage, leading to higher costs and decreased access to needed services. Fortunately, there are resources and tips to help protect your Medicare benefits. It’s crucial to understand how prevention tools, educational services, and vigilant providers work together to safeguard your coverage within the Medicare program. Awareness is your first line of defense, and knowing what steps to take can empower you to detect and prevent abuse. By utilizing available resources, you can take proactive measures to ensure your Medicare services remain secure and reliable.

Tips to Protect Yourself and Your Coverage

To guard against Medicare abuse, being informed is essential. Start by reviewing your Medicare Summary Notices regularly. These notices detail the amounts received and the amounts billed to Medicare. Look for any unfamiliar services or charges that could indicate abuse. If something seems off, contacting your healthcare provider first to clarify is prudent. They can correct errors or explain legitimate charges. Additionally, never share your Medicare card or personal information with strangers, as this can lead to identity theft and unauthorized use of your Medicare benefits.

Enlisting the support of trusted resources can further shield your Medicare coverage. The Senior Medicare Patrol (SMP) program is a wonderful resource that educates and empowers Medicare beneficiaries. They can help you understand potential scams and report them. Online resources, workshops, or hotlines come in handy for learning more about protecting your Medicare benefits. Remember, staying informed about your Medicare program and familiarizing yourself with what constitutes abuse are powerful tools in prevention.

Moreover, ensuring you’re working with reputable healthcare providers is key. Choose providers who value transparency and are committed to ethical billing practices. If you suspect Medicare abuse, reporting it promptly to Medicare’s official centers or the Office of Inspector General helps protect not only your coverage but also the integrity of the broader Medicare system. By following these tips, you can confidently navigate your healthcare with security and peace of mind.

Thank you for exploring these common Medicare questions with us. To find the Medicare plan that fits your needs, enter your ZIP code on our site. You can compare benefits, costs, and options with ease. We’re here to support you and provide guidance whenever needed. Once our phone number is available, feel free to call for personalized help on your Medicare journey. Your understanding and comfort with Medicare are our priorities.

Compare plans and enroll online

Frequently Asked Questions

What does Medicare Part A and Part B cover?

Medicare Part A covers inpatient hospital stays, care in a skilled nursing facility, hospice care, and some home health care. Part B is for outpatient services such as doctor visits, outpatient care, and preventive services.

When does Medicare Open Enrollment occur?

The Medicare Open Enrollment Period runs annually from October 15 to December 7. During this time, you can review and make changes to your Medicare plans to better fit your healthcare needs and budget.

How do Medicare Advantage and Medigap differ?

Medicare Advantage plans, offered by private companies, bundle Part A and Part B coverage and usually include additional benefits like dental and vision. Medigap, however, helps with out-of-pocket costs not covered by Original Medicare, like copayments and deductibles.

What does Medicare Part D cover?

Medicare Part D helps cover prescription drug costs. It is offered by private companies and varies by premiums, copayments, and drug coverage. Consider your medication needs and available plans in your area to find the right fit.

What should I understand about Medicare and Medicaid?

Medicare primarily assists those 65+ and certain younger individuals with disabilities, focusing on hospital and outpatient services. Medicaid, aimed at low-income individuals, offers broader coverage, including services often beyond Medicare’s scope.

Have Questions?

Speak with a licensed insurance agent

1-855-398-0716

TTY users 711

Mon-Fri: 8am-9pm ET

Find & Compare Plans Online

ZRN Health & Financial Services, LLC, a Texas limited liability company

Russell Noga is the CEO of ZRN Health & Financial Services, and head content editor of several Medicare insurance online publications. He has over 18 years of experience as a licensed Medicare insurance broker helping Medicare beneficiaries learn about Medicare, Medicare Advantage Plans, Medigap insurance, and Medicare Part D prescription drug plans.