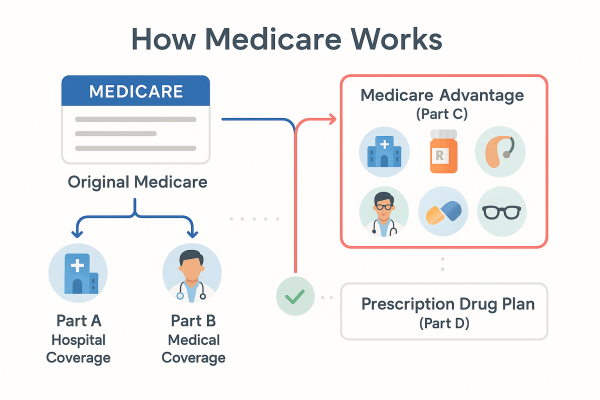

Taking the leap to explore Medicare plans doesn’t have to be stressful. The first step is understanding what each plan offers in terms of coverage, services, and costs. Original Medicare might seem straightforward with its Parts A and B, but you’ll need to decide if adding a Medicare Supplement, also known as Medigap, enhances your coverage.

These policies help cover costs that Original Medicare doesn’t, like deductibles and coinsurance.

Evaluating Medicare Advantage plans is another key step. These plans often include extra benefits like vision, dental, and hearing services. They may also pack in drug coverage, making them a complete package for those wanting consolidated care.

To start your exploration, make a list of your current healthcare needs, including any required services or medications.

This list will help you match your needs with a plan that offers the right coverage. Consider the network of providers covered by each plan, especially if you want to keep your current doctors. Seeking a plan with a wide network might increase your care options. As you compare options, look closely at costs such as premiums, deductibles, and co-payments, as these will affect your budget.

Each plan’s policy may vary, so be sure to read the fine print on services covered.

Don’t forget about Part D for drug coverage. Many Advantage plans include this, but stand-alone Part D plans also exist if Original Medicare is your primary choice. List the medications you take and check if they’re covered under each plan’s formulary.

Ensuring your drugs are covered reduces out-of-pocket expenses. Engaging with educational resources like MedicarePlansGuide.org can further assist your understanding.

There, you can learn more about each plan in detail.

Finally, remember that your needs might change over time, so stay flexible. Annual enrollment periods are a chance to reassess and switch plans if necessary. Learning how to explore and compare Medicare options sets a solid foundation for making informed decisions, helping you manage your healthcare with confidence.

Enter your ZIP code on our website to compare Medicare options, and feel free to seek personalized help as soon as our phone support becomes available.

Understanding Medicare can seem complex, but you don’t have to navigate it alone. Our goal is to help seniors and caregivers feel informed and confident. By exploring Medicare Parts A, B, C, and D, you gain valuable insights into which options may fit your needs.

We invite you to enter your ZIP code on our site to compare Medicare options in your area. For more personalized assistance, you can call us once our phone number is available. We’re here to provide the support you need on your Medicare journey.