Medicare Supplement Plan N, commonly called Medigap Plan N, is a popular option for individuals enrolled in Original Medicare who want meaningful gap coverage with lower monthly premiums than some more comprehensive Medigap plans. It provides strong financial protection while allowing for modest cost sharing in certain situations.

What Is Medicare Plan N?

Medicare Plan N is a standardized Medicare Supplement policy offered by private insurance companies to work alongside Original Medicare Part A and Part B. Original Medicare generally pays a large portion of approved healthcare costs, but beneficiaries remain responsible for deductibles, copayments, and coinsurance.

Plan N helps reduce those out-of-pocket expenses while keeping premiums relatively competitive.

Like other Medigap plans, Plan N does not replace Original Medicare. Instead, it supplements coverage administered by Medicare, helping pay certain costs that Parts A and B leave behind.

Benefits and Coverage of Medicare Plan N

Medicare Plan N includes a broad set of core benefits, making it a strong choice for individuals who want reliable coverage with some flexibility:

-

Part A hospital coinsurance and hospital costs, including coverage for up to 365 additional hospital days after Medicare benefits are used.

-

Part B coinsurance helps pay for outpatient services such as doctor visits and medical procedures.

-

Skilled nursing facility coinsurance can significantly reduce costs during recovery or rehabilitation.

-

Part A hospice care coinsurance or copayments, supporting comfort-focused care when needed.

-

Foreign travel emergency coverage, subject to plan limits, for medical emergencies outside the United States.

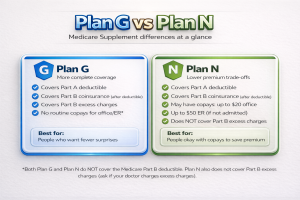

Unlike some other Medigap options, Plan N does not cover the Medicare Part B deductible or Part B excess charges.

Beneficiaries may also have small copayments for certain office visits and emergency room visits when not admitted.

Why Some Beneficiaries Choose Plan N

Plan N often appeals to individuals who are generally healthy, do not expect frequent medical visits, or are comfortable with limited copayments in exchange for lower premiums.

The cost-sharing structure can make monthly expenses more predictable while still protecting against major medical costs.

Because Medigap plans are standardized, the medical benefits of Plan N are the same regardless of the insurance company offering it. Premiums, customer service, and pricing stability are typically the main factors that differ between insurers.

Final Thoughts

Medicare Supplement Plan N offers a practical balance between coverage and affordability.

By covering many of the major gaps in Original Medicare while allowing limited copayments, Plan N can be a cost-effective option for individuals seeking dependable supplemental coverage without paying higher premiums for more comprehensive plans.