Once you’ve weighed the differences between Medigap Plan G and Plan N, the next step is to carefully consider your specific health needs, budget, and preferences. Beginning with the coverage offered, contemplate how each Medigap policy aligns with your healthcare usage.

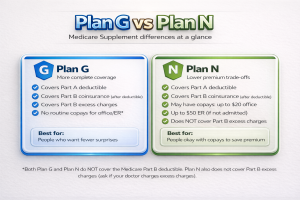

If you frequently visit doctors or require regular medical services, Plan G’s comprehensive nature might provide greater peace of mind by covering most out-of-pocket expenses, save for the Part B deductible. Conversely, if you’re comfortable with cost-sharing in the form of copayments and prefer lower premiums, Plan N could be a more viable option.

Evaluating your current health status and anticipating potential future medical needs is crucial. Consider whether the benefits each plan offers, such as deductible coverage, will accommodate your personal circumstances.

It’s also wise to review how each plan handles coinsurance and any possible rate increases that could impact your long-term affordability. Remember that a medigap plan not only supplements Original Medicare but also empowers you to choose any healthcare provider that accepts Medicare, enhancing your flexibility and control over your healthcare decisions.

Take into account the enrollment period as well. The best time to purchase a Medigap policy is during the initial six-month enrollment period starting when you first enroll in Medicare Part B. During this period, you can buy any plan without facing medical underwriting, meaning your health status won’t affect your rate.

Missing this window might result in higher rates or even denial of coverage based on pre-existing conditions. Carefully comparing the plan benefits, coverage, and rates helps ensure you’re selecting a plan that matches both your healthcare needs and financial expectations.

Finally, remember that making an informed choice extends beyond immediate savings, it’s about ensuring stable, predictable healthcare costs in retirement. To explore Medicare options further, remember to enter your ZIP code on our site.

We’re here to guide you by offering detailed insights into available plans and services. Our educational resources are designed to empower you in making confident, well-informed decisions about your health insurance coverage.

After reviewing both Medigap Plan G and Plan N, you may feel ready to compare your options further. Remember, it’s important to match a plan to your personal healthcare needs and budget. Use our site to enter your ZIP code and explore Medigap choices in your area.

We’re here to help simplify decisions and ensure you’re informed about your Medicare options. You can also call us for personalized guidance when our phone service is available. Empower yourself with clear, supportive information and the confidence to choose what’s right for you.