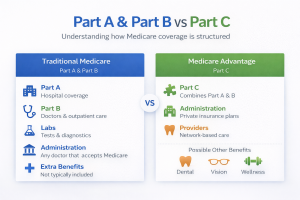

Medicare consists of several distinct parts, each serving a unique role in providing healthcare coverage for seniors. Medicare Part A covers hospital stays, skilled nursing facility care, hospice care, and some home health care.

Typically, most people don’t have to pay a premium for Part A if they or their spouse paid Medicare taxes while working.

Medicare Part B, on the other hand, covers outpatient care, doctor services, and preventive services, and most beneficiaries pay a standard premium.

However, your Modified Adjusted Gross Income (MAGI) can lead to higher premiums due to the Income-Related Monthly Adjustment Amount (IRMAA).

For those who are eligible, Medicare Part C, or Medicare Advantage, offers an alternative, often bundling services found in Part A, B, and sometimes D into one plan.

Understanding how each Medicare part integrates with your income level can be crucial, especially when these parts include expense adjustments or tax considerations.

Finally, Medicare Part D provides prescription drug coverage and can be critical for seniors managing healthcare costs. Like Part B, Part D premiums are influenced by your income, with higher earners facing the same IRMAA adjustments.

Familiarizing yourself with these Medicare parts enables you to evaluate your healthcare needs efficiently, aligning benefits and costs to your financial situation.