Understanding your Medigap plan options is crucial for making informed decisions about your healthcare coverage. Medigap Plan G and Plan G High Deductible are two popular choices for supplementing Medicare in 2026. Each offers different benefits and costs, tailored to suit varying needs and budgets. This page will help you discover the key differences between these plans, ensuring you are well-equipped to choose what works best for your healthcare needs. Whether you are new to Medicare or exploring supplement options, this guide simplifies the comparison between these important Medigap plans and who sells Medigap insurance.

Compare Medicare Plans

Compare plans and costs in your area

Medigap Plan G vs Plan G High Deductible

Key Highlights

- Medigap Plan G offers comprehensive coverage, bridging the gap for costs not fully covered by Original Medicare.

- Plan G covers Part A deductibles, Part B coinsurance, and emergency care during overseas travel.

- High-deductible plans trade lower premiums for higher out-of-pocket costs before coverage begins.

- Choose high deductibles for lower premiums, ideal for healthy seniors with fewer medical visits.

- Enrolling in Plan G during the open enrollment period avoids medical underwriting challenges later.

Compare plans and enroll online

Understanding Medigap Plan G

Medigap Plan G is a popular Medicare supplement insurance option that offers extensive benefits for seniors looking to cover healthcare costs not paid by Original Medicare. Known for its comprehensive coverage, Plan G helps bridge the gap by covering many out-of-pocket expenses such as co-pays and coinsurance. In this section, we’ll delve into what Plan G covers, its benefits, and the costs associated with this Medicare supplement plan. With this understanding, seniors can compare Medigap options and decide if Plan G aligns with their healthcare needs and budget.

What Plan G Covers and Benefits

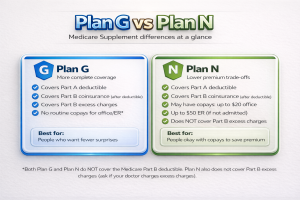

Medigap Plan G is designed to supplement Original Medicare by covering a wide range of health expenses that Medicare doesn’t fully pay for. One of the significant benefits of Plan G is that it covers Part A deductible costs, which includes hospital stays and skilled nursing facility care. When you’re hospitalized, Medicare typically requires you to pay a deductible before Medicare pays its share. Plan G steps in to cover these deductible costs, easing the financial burden on your health expenses.

Moreover, Plan G also covers Part B coinsurance and co-payments. Part B is where many outpatient services, like doctor visits and preventive services, fall under. Without a Medigap plan, you’d typically pay 20% of these costs out-of-pocket, but with Plan G, these expenses are covered. Additionally, it includes coverage for blood, under Part B, the first three pints of blood are covered each year, which can be crucial for those needing frequent transfusions.

Another benefit of Plan G is the coverage for foreign travel emergency care, offering peace of mind for retirees who travel abroad. This supplement offers up to 80% coverage for emergency medical care incurred during overseas trips, which can be a crucial advantage for travel-inclined seniors. This coverage helps negate the worry of healthcare expenses during travel, which Original Medicare alone wouldn’t handle as effectively.

Importantly, Plan G does not cover the Part B deductible, so you’ll need to pay the annual deductible out-of-pocket. Despite this exclusion, many find the broad benefits of Plan G, like skilled nursing facility care coverage and excess charges protection, to be valuable and worthwhile. As you review supplement insurance options, consider how Plan G aligns with your medical needs and budget for a well-rounded approach to healthcare coverage.

I am text block. Click edit button to change this text. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

Costs Associated with Medigap Plan G

The costs associated with Medigap Plan G involves monthly premiums, which can vary widely depending on several factors. These factors include your geographic location, age, gender, and tobacco use. On average, seniors can expect their Medigap Plan G premiums to be on the higher side compared to other plans due to the comprehensive coverage it offers.

While monthly premiums may seem like a significant expense initially, it’s important to weigh these costs against the out-of-pocket expenses Plan G covers. For instance, by covering the costly Part A deductible and coinsurance, along with Part B excess charges, Plan G helps minimize unexpected healthcare costs. This can be especially beneficial for those with chronic conditions or frequent medical needs, as the policy aids in managing and predicting healthcare expenses.

When considering the cost, it’s also crucial to look at the potential savings during medical emergencies or frequent healthcare visits. Although Plan G doesn’t cover the Part B deductible, many seniors find the predictable and lower cost-sharing for other services balances out this gap. Also, the peace of mind provided by the wide-ranging protection of Plan G is a significant factor contributing to its popularity among Medicare enrollees.

Understanding and planning for these costs involves outlining your healthcare needs and budgeting accordingly. It’s beneficial to compare Medigap rates annually since premiums can change, affecting your budget. When evaluating options, consider both the premiums and other out-of-pocket costs that might arise, such as deductibles not covered by Plan G. Taking a strategic approach will ensure that you choose a suitable medigap plan that aligns both with your financial means and health care needs.

Lastly, before enrolling, it’s advisable to review the policy thoroughly, understanding both the costs and benefits it entails. Each insurance company may price their plans differently, even for the same coverage. Thus, comparing Medigap policies, including Plan G, through resources like MedicarePlansGuide.org can be helpful. These comparisons serve to empower your decision-making process, ensuring your Medicare supplement choice affords you the fullest coverage at a manageable cost.

Exploring High Deductible Plan Options

Understanding Medigap plans can be a journey, but knowing the ins and outs of high deductible plans, like Plan G and its high-deductible version, is crucial for making informed decisions about your healthcare costs. These plans work to offer the comprehensive coverage of standard Medigap options while providing a more affordable route through lower monthly premiums in exchange for a higher deductible. We’ll explore how these high-deductible plans operate, the coverage they provide, and why some might opt for such plans despite the higher initial out-of-pocket costs.

How High Deductible Plans Operate

A high deductible plan, particularly with Medigap, often serves as an interesting choice for those looking to balance comprehensive Medicare coverage with affordability. These plans essentially work by allowing enrollees to pay lower premiums compared to standard Medigap plans like Plan G. However, they require paying more out-of-pocket before insurance benefits kick in , this is your deductible amount. The high deductible Medigap Plan G stands out as it covers the same medical benefits but requires reaching a set deductible before coverage begins.

During 2026, the deductible amount for high deductible plans may see adjustments, reflecting changes in healthcare costs and regulations. It`s important to stay informed about these updates to better understand the financial commitment involved. Once you’ve met your deductible, the plan operates like any other Medigap plan, offering supplemental insurance to aid with various out-of-pocket costs not covered by traditional Medicare. This includes copays, coinsurance, and certain deductibles, ensuring that once the high-deductible threshold is met, beneficiaries get nearly the same range of benefits as regular Plan G.

Another point to consider is how these plans manage costs over time. High deductible plans are often chosen for their lower monthly premiums. Since you pay less monthly, it could look like affordable care compared to plans with higher premiums but lower deductibles. However, you must be prepared for the potential upfront costs in case of a health event requiring immediate medical attention. These plans offer excellent options for relatively healthy adults who expect fewer healthcare needs during the year as they trade initial savings for potential higher payments later, should care be required.

Finally, understanding the operations of a high deductible plan is crucial for making the right insurance decision. It involves weighing your current health situation, your financial capability to meet high out-of-pocket costs, and your comfort level with spending more when healthcare events occur. This strategic analysis helps in aligning your plan choice with your healthcare needs effectively while considering exercises in cost-saving through lower premiums.

Why Choose a High Deductible Plan?

Deciding whether a high deductible Medigap plan is right for you often comes down to your personal financial situation and health care needs. One compelling reason seniors might choose a high deductible plan is the appeal of lower monthly premiums. Lower premiums can offer significant savings if medical expenses remain low throughout the year, presenting a feasible way to manage health insurance costs while still ensuring extensive insurance coverage when necessary.

For those who are generally healthy and foresee lower medical expenses, the prospect of saving on monthly insurance can be attractive. It allows for allocating funds elsewhere in the budget. Those planning for unexpected health events, albeit fewer, can also appreciate the back-up protection these plans provide after the deductible amount is met. As with any policy, it involves a balance of potential risk versus reward; but the plan benefits after the deductible can offer substantial coverage to offset large medical bills, making it a viable choice for many.

Additionally, considering the increasing costs of traditional Medicare and supplemental insurance, a high deductible plan can provide a unique peace of mind. You’ll have comprehensive protection, bridging coverage gaps left by Original Medicare once the deductible is reached. The insurance plan becomes a fiscal safeguard, especially for occasional travelers or those nearing retirement who are still in good health.

Choosing a high deductible plan also allows for more straightforward budgeting and a structured approach to managing healthcare spending. Knowing the deductible and monthly premiums upfront helps in planning healthcare budgets annually, offering predictability in spending. This form of coverage might suit those looking to retire soon or manage healthcare on a fixed income, as it provides control over how much is paid each month with an understanding of potential out-of-pocket costs when medical care is needed.

Ultimately, the decision to enroll in a high deductible Medigap plan should be informed by individual healthcare needs, financial comfort, and the capacity to handle higher out-of-pocket expenses should they arise. Always ensure that a thorough evaluation of current and projected health could help make a confident choice when considering these plans.

Comparing with standard Medigap plans through resources that offer comprehensive analysis, like MedicarePlansGuide.org, can empower you to choose the coverage that best fits your lifestyle and financial situation. Once our phone number is available, don’t hesitate to call for personalized help.

Introducing High-Deductible Medigap Plan G

High-Deductible Medigap Plan G is becoming an attractive option for those seeking a balance between comprehensive healthcare coverage and affordability. This plan offers similar benefits to the Standard Plan G, but it comes with a higher deductible.

By choosing this high-deductible option, individuals can enjoy lower monthly premiums, benefiting those on a budget or with minimal healthcare needs. We’ll explore the specifics of its coverage features, how it compares to standard Plan G, and why it might be a fitting choice for some seniors looking for cost-effective health insurance solutions in 2026.

| Plan Type | Premiums | Deductibles | Coverage Features | Ideal For |

|---|---|---|---|---|

| High-Deductible Plan G | Lower Monthly Premiums | High Deductible Required | Comprehensive Coverage After Deductible | Individuals Seeking Lower Monthly Costs |

| Standard Plan G | Higher Monthly Premiums | No Deductible | Comprehensive Coverage from Start | Individuals Preferring No Out-of-Pocket Deductible |

This table outlines the primary contrasts and parallels between High-Deductible Medigap Plan G and Standard Plan G, helping to clarify considerations for prudent healthcare choices in 2026.

Coverage Features of High-Deductible Medigap Plan G

High-Deductible Medigap Plan G provides several benefits similar to the standard Plan G, making it a suitable choice for those who want to maintain a broad scope of insurance coverage. Like its standard counterpart, this plan helps cover many expenses that Original Medicare doesn’t fully pay for, including copayments and coinsurance associated with Part A and Part B. One standout feature is the coverage for Part A coinsurance and hospital costs up to an additional 365 days after Medicare benefits are exhausted, ensuring substantial hospital care protection.

However, what sets the high-deductible version apart is the upfront deductible cost, a set amount you’ll need to pay before any benefits kick in, acting as the gateway to your coverage. For many seniors, especially those in relatively good health, the lower monthly premiums of this high-deductible plan can translate into significant annual savings. This feature provides an advantageous balance , affordable coverage upfront with more substantial financial responsibility only taking effect when health needs arise.

This plan is particularly beneficial for retirees who travel abroad, as it includes foreign travel emergency care coverage, something that’s not automatically covered by Original Medicare. Up to 80% of the cost for emergency medical treatment during overseas travel is covered, offering peace of mind to those adventure-bound retirees. Additionally, skilled nursing facility care and blood transfusions are among the health expenses cushioned by this coverage, both of which could otherwise become hefty out-of-pocket payments.

It`s also vital to understand that, despite the high deductible, once this threshold is met, the plan covers almost all of the same benefits as standard Plan G, without further out-of-pocket costs for covered services within that policy year. Therefore, seniors choosing this policy will find it valuable if enrolled with a clear understanding of their healthcare expenses and the risks they`re willing to manage. This approach can help make the most of the benefits and cost-effectiveness of a high-deductible plan.

Find & Compare Plans Online

Comparing High-Deductible Medigap Plan G and Standard Plan G

When comparing the High-Deductible Medigap Plan G with the Standard Plan G, the most notable difference is the cost structure. While both plans offer comprehensive Medigap coverage, the high-deductible version is known for its lower monthly premiums, which can be appealing in managing fixed incomes. This is a key difference, the standard Plan G typically requires higher insurance premiums because there`s no deductible threshold.

The primary similarity between these plans lies in the breadth of benefits they furnish once applicable costs are met. Both cover excess charges from Part B, and neither covers the Part B deductible itself. This means once the deductible is paid with the high-deductible version, your coverage functions very similarly to the standard plan, encompassing medical services such as doctors visits, outpatient surgery, and other essential healthcare services without additional charges.

Standard Plan G suits individuals who expect regular care each year, as it doesn’t involve the hurdle of meeting a deductible upfront. This makes it ideal for those who prefer to manage their healthcare spending incrementally through regular premium payments. Conversely, the high-deductible option hones in on those looking for economical solutions who may need to budget their healthcare expenses by focusing on lower monthly payments in exchange for a higher deductible.

Since 2026 may bring shifts in healthcare costs, projecting out-of-pocket expenses against potential benefits is crucial. Seniors should weigh their current health status, anticipated medical expenses, and readiness to cover a high deductible during emergencies with the benefits of potentially reduced rates. For many, the decision comes down to financial flexibility and healthcare needs, both immediate and projected.

Ultimately, the decision to choose between these plans should involve a thorough evaluation of personal circumstances, and financial foresight, and leveraging insights from comparative resources like MedicarePlansGuide.org can empower more informed decisions. Always explore your options thoroughly, ensuring the chosen plan aligns well with your healthcare strategies for today and into 2026.

Considering a Deductible Plan for 2026

As 2026 approaches, many are exploring the idea of deductible plans to manage healthcare costs effectively. Choosing the right Medigap plan is crucial, particularly when considering options like Plan G and its high-deductible counterpart. These plans aim to balance comprehensive insurance coverage with affordability.

Understanding the eligibility requirements, enrollment process, and evaluating the potential costs and benefits is essential for making informed decisions. This section provides guidance on how eligible seniors can enroll in high-deductible plans and examines how deductible amounts impact overall costs.

Eligibility and Enrollment for High Deductible Plan G

Eligibility for Medigap Plan G, and its high-deductible variant, often requires understanding both the Medicare enrollment rules and additional Medigap regulations. Generally, to enroll in a high-deductible Plan G, you must first be enrolled in Medicare Parts A and B. Eligible individuals are typically those who are turning 65 and are newly eligible for Medicare, or those already on Medicare who are looking to switch Medigap plans.

It`s also crucial to note that while Medicare has no open enrollment period for Medigap plans, your best opportunity to apply without medical underwriting is during your six-month Medigap Open Enrollment Period, which starts the month you turn 65 and are enrolled in Part B.

During this time, insurance companies cannot refuse you a policy based on health conditions, nor charge more. However, waiting beyond this period can make it harder to get a plan, especially if you have pre-existing conditions. While typical Medicare Advantage plans operate with specific enrollment windows each year, Medigap plans do not, making it essential to plan ahead and know your unique eligibility timing and the steps required for enrollment.

To begin the enrollment process, you`ll need to contact the insurance company offering the Medigap policy you’re interested in. It can be helpful to consult with a Medicare expert who can guide you through the nuances of high-deductible Plan G, advise on rates and costs associated with different insurers, and elucidate the benefits that accompany your chosen plan. You’ll want to gather information, compare policies, and confirm your eligibility status before making a decision. Resources like MedicarePlansGuide.org can simplify this process by aiding in comparing different Medigap options tailored to fit varying healthcare needs and budgets.

Additionally, it`s essential always to review plan details, benefits, and costs regularly. This ensures the plan you choose aligns with your finances and healthcare requirements, especially when plans change or new options become available in 2026. Discuss ongoing health needs with a healthcare adviser to understand how a high-deductible Plan G could fit into your Medicare strategy. Knowledge and planning are your strongest tools in ensuring you receive the coverage you need at a price that makes sense.

Evaluating the Deductible Amount and Costs

Evaluating the costs of a high-deductible Medigap Plan G involves assessing both the deductible amount and the associated premiums. The deductible amount is the out-of-pocket expense threshold you must meet before the plan begins paying for benefits. For many seniors, the appeal of a high-deductible plan lies in its lower monthly premiums, which can make it a cost-effective choice for those with limited healthcare needs.

As healthcare costs are predicted to change by 2026, understanding and comparing deductibles is critical. Initially, paying higher out-of-pocket costs may seem daunting, but for relatively healthy individuals, the accumulated savings through lower premiums can outweigh this initial expenditure. It’s about balancing immediate cost savings against the potential financial burden if significant medical care is required.

Consider, for instance, the way high-deductible plans translate to financial planning. These plans require a clear understanding of your health history and anticipated medical needs. If you don`t expect frequent doctor visits or high medical bills, the high deductible can work in your favor, providing coverage once you meet the threshold while keeping monthly expenses manageable. On the other hand, seniors with regular healthcare needs might find the standard Plan G predictable premiums more favorable, despite its higher cost.

It`s also important to evaluate your comfort level with risk. Some beneficiaries may prefer paying more up front to lower their monthly payments, while others might lean towards plans with lower deductibles to reduce unforeseen expenses. Calculating potential annual medical costs, including out-of-pocket expenses and the expected deductible, offers a clearer picture of budgetary impacts and helps guide the decision-making process.

Ultimately, evaluating these factors helps ensure that seniors choosing Medigap coverage can tailor their insurance policy to fit their health and financial situation. Keep in mind the possibility of changes in Medicare regulations or healthcare costs, as these could adjust plan details and benefits. Continuous review and engagement with resources like MedicarePlansGuide.org help you stay informed, allowing a more strategic approach to selecting the right Medigap plan for your individual circumstances.

Take the next step in exploring your Medicare coverage with confidence. Enter your ZIP code on our site to compare the Medigap options available for 2026. Once our phone number is available, feel free to call for personalized assistance, ensuring your Medicare coverage aligns perfectly with your needs.

To strategically select a high-deductible Medigap Plan G, consider a few more important tips:

- Research historical changes in Medicare regulations before finalizing your decision. Understanding how Medicare has evolved over time can provide insights into potential future shifts that may affect your coverage needs.

- Factor in family health history when assessing future medical needs. If certain conditions tend to run in your family, it could be wise to anticipate these in your medical coverage planning.

- Utilize online resources for comparing different plan options in your area. Websites and comparison tools can offer an easy way to evaluate how various plans differ in terms of cost and coverage.

- Consider potential lifestyle changes that may affect healthcare requirements. Whether it’s a move to a different climate, a change in diet, or new exercise habits, lifestyle changes can influence your health needs over time.

- Periodically review your plan to ensure ongoing suitability with health status. As health conditions can change, it’s important to regularly assess whether your current Medigap plan still meets your requirements.

- Budget for potential medical expenses alongside regular monthly commitments. Having a clear picture of all your expenses can help you determine how much risk you can afford with a high-deductible plan.

- Engage with insurance experts for tailored advice on your Medigap selections. Insurance professionals can offer personalized guidance, helping you choose a plan that aligns with your specific situation.

Keeping these considerations in mind can significantly aid in choosing a Medigap plan that fits both your health and financial needs effectively.

To explore Medigap Plan G and Plan G High Deductible for 2026, enter your ZIP code on our site. This helps you compare options and coverage costs more easily. Our resources are here to guide you through finding the right coverage. Feel free to contact us for personalized assistance when our phone number becomes available. We aim to make Medicare choices simpler for you. Remember, understanding your coverage options can bring peace of mind.

Compare plans and enroll online

Frequently Asked Questions

What are the key differences between Medigap Plan G and Plan G High Deductible?

Medigap Plan G offers comprehensive coverage, including Part A deductibles, Part B coinsurance, and more, with higher premiums but lower out-of-pocket costs. The High Deductible Plan G provides the same benefits but requires you to meet a higher deductible before the plan starts paying, in exchange for lower premiums. This option suits healthy seniors with fewer medical visits.

What benefits does Medigap Plan G cover?

Medigap Plan G covers several key expenses: Part A deductible costs for hospital stays, skilled nursing facility care, and Part B coinsurance for outpatient services. Additionally, it includes foreign travel emergency care, covering up to 80% of emergency medical expenses while traveling abroad, along with the first three pints of blood each year under Part B.

What should I consider when choosing a High Deductible Medigap Plan G?

When opting for a High Deductible Plan G, consider your health status, financial capability to meet higher out-of-pocket expenses, and comfort level with paying a larger share upfront for medical services. This plan suits lower annual health expenses, providing extensive coverage after the deductible has been met.

How does enrolling during the Medigap Open Enrollment Period benefit me?

Enrolling during your six-month Medigap Open Enrollment Period, starting the month you turn 65 and are enrolled in Part B, allows you to apply without medical underwriting challenges. This means you can’t be denied coverage or charged extra due to health conditions, enhancing your opportunities to secure the plan that fits your needs.

Can I switch from a standard Plan G to a High Deductible Plan G?

Switching from a standard Plan G to a High Deductible Plan G involves checking your eligibility and your insurance company’s rules. It might require medical underwriting, where your health status is evaluated, unless you’re switching during specific enrollment periods with guaranteed issue rights. Consulting a Medicare expert can clarify this transition for you.

Have Questions?

Speak with a licensed insurance agent

1-855-398-0716

TTY users 711

Mon-Fri: 8am-9pm ET

Find & Compare Plans Online

ZRN Health & Financial Services, LLC, a Texas limited liability company

Russell Noga is the CEO of ZRN Health & Financial Services, and head content editor of several Medicare insurance online publications. He has over 18 years of experience as a licensed Medicare insurance broker helping Medicare beneficiaries learn about Medicare, Medicare Advantage Plans, Medigap insurance, and Medicare Part D prescription drug plans.